Borderless electricity: completing the internal energy market

by Georg Zachmann on 5th September 2013

After the European Commission in November last year and the European Council in May, it is now up to the European Parliament to affirm its commitment to make the internal energy market work. The vote on a corresponding report prepared by Jerzy Buzek is scheduled on September 10th. The report highlights important deficits of the internal energy market and presents numerous suggestions on how to address them. In preparation for this report, Bruegel has been requested to prepare a background document that quantifies the benefits of the internal market and proposes a blueprint for overcoming them.

Extending and deepening the internal electricity market is beneficial

A comprehensive quantification of the benefits of a genuine internal electricity market does not exist. However, empirical case studies and simulations suggest that additional integration steps – such as integrating balancing and reserve markets – promise significant yet unexploited benefits. The competition-enhancing effects of market integration are also not yet fully exploited. Furthermore, the infrastructure for cross-border electricity exchanges is increasingly a bottleneck. The cost of using major cross-border transmission lines increased by more than 10 percent between 2012 and 2013 to about €1 billion.

Consequently, there are significant benefits to be had from extending the internal electricity markets by integrating all electricity market segments and deepening it by removing administrative and physical barriers to cross-border electricity exchanges.

Benefits depend on who integrates and how integration is organised

We find that the benefits strongly depend on the systems‘ characteristics and the approach taken to integration:

- First, substantial efficiency gains of international electricity trade can already be reaped at limited levels of interconnection (5 percent). As the benefits of resolving the very last transmission constraints are very small, the optimal level of transmission investment will not result in an unconstrained network.

- Second, ‘shallow market integration,’ which only targets optimised usage of the existing system, provides significantly lower benefits than ‘deep market integration,’ which allows for a reconfiguration of the joint power plant fleet including mutual dependence.

- Third, the benefits of market integration increase with the capacity of renewables. If renewable electricity generation capacities are doubled from current levels the efficiencies increase disproportionally. Consequently, the ambitious European renewables targets will justify greater cross-border transmission capacity.

- Fourth, distant countries with high shares of uncorrelated renewables benefit most from market integration. Limiting market integration to regions with similar renewables production patterns means missing out on substantial trading benefits.

- Fifth, there are significant redistributive effects when countries‘ power plant fleets are optimised in an integrated way. The balance between consumers and producers is shifted, certain power plants become redundant and countries become mutually dependent. Depending on the level of integration, different generation technologies are preferable.

Market integration requires political intervention for four reasons:

- First, electricity networks are a natural monopoly that requires public intervention to produce socially desirable results.

- Second, the actions of individual market participants have significant externalities that affect all other participants. Because those externalities cannot be dealt with (internalised) by vertical integration, public intervention is necessary to achieve socially desirable sector structures.

- Third, in EU member states very different market arrangements have emerged. Those arrangements are a priori largely incompatible across borders and trading thus requires interfaces, which are highly complex because of the need to make different energy products seamlessly tradable between more than 30 incompatible markets. The solution to this – harmonised rules – has significant redistributive effects for market participants. Public intervention is required to strike stable arrangements.

- Fourth, energy is a strongly politicised product in all countries. Consequently, self-organisation of cross-border markets is politically constrained.

Quantifying the infrastructure need

There are numerous exercises quantifying the future need for energy infrastructure in Europe. The infrastructure needs they predict differ markedly because the ‘optimal network’ depends strongly on the assumptions made. These assumptions imply societal choices: How are the different objectives of network investments weighted? How will energy demand develop? Which technologies does the model include? How will the cost and availability of these technologies develop? Consequently, the process used to determine the ‘optimal network’ is more important than the numerical outcomes of individual studies.

Market design not adapted to the changing environment

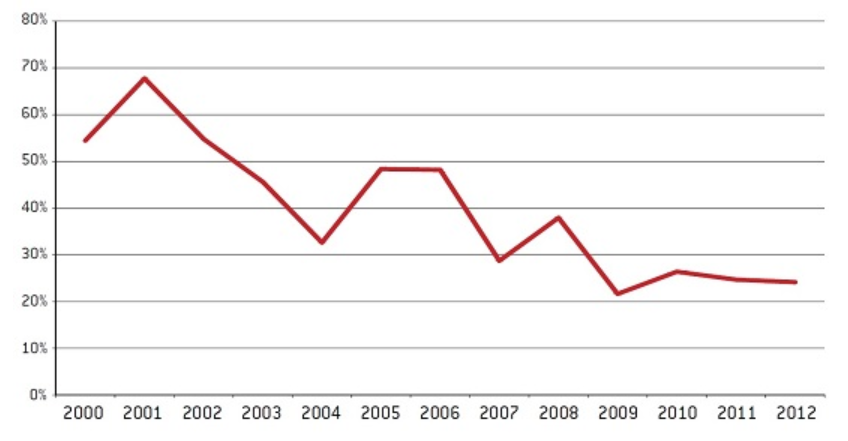

The liberalisation of electricity generation and retail businesses, and the long-term shift in the generation structure towards variable renewables, is changing the electricity market environment. The value of electricity is more and more determined by factors such as capacity, ancillary services, location and ‘greenness’, which are remunerated through national schemes. At the same time the value of the component traded at European level – wholesale electricity and emission allowances – has decreased sharply (for an illustration, see Figure 1 for Germany).

Source: Bruegel based on IEA and EEX.

Thus, the incentives for investment in the electricity system are becoming more and more driven by national administrative choices. The EU ‘Target Model’ that should be implemented by 2014 does not address the issue of establishing European markets for capacity, ancillary services, location and ‘greenness’. Consequently, the system under which these services are remunerated will matter more for an investor/operator than the location at which they could be economically provided.

Current infrastructure planning does not target European welfare maximisation

Most transmission line investments in Europe continue to be based on national plans, that target domestic welfare maximisation or network cost minimisation, and are funded by domestic network users. This model fails in the international or cross-border context because both domestic and cross-border transmission lines cause significant spillovers onto neighbouring countries’ networks that are not properly addressed in national plans.

As a consequence, cross-border transmission capacity has not been substantially increased in the past five years. Previous European schemes lacked the system-wide overview and were either underfunded or too short-term. The European Union infrastructure package[1] is intended to deliver more cross-border electricity transmission. The cross-border cost-allocation method that it foresees could become quite powerful – but for the time being is only concentrated on a limited number of politically-selected individual projects.

Overall, network planning continues to be driven by the transmission system operators (TSOs), which monopolise the information about the technical details of the energy system, but which have incentives that are not necessarily aligned with societal objectives. The EU infrastructure package is an extension of the current system of national-welfare centred regulations, a system which does not target the optimisation of the EU electricity network, and as such is inconsistent with a truly single market.

Proposal

The most straightforward European single energy market design would entail a European system operator regulated by a single European regulator. This would ensure the predictable development of rules for the entire EU, significantly reducing regulatory uncertainty for electricity sector investments. But such a first-best market design is unlikely to be politically realistic in the European context for three reasons. First, the necessary changes compared to the current situation are substantial and would produce significant redistributive effects. Second, a European solution would deprive member states of the ability to manage their energy systems nationally. And third, a single European solution might fall short of being well-tailored to consumers’ preferences, which differ substantially across the EU.

To nevertheless reap significant benefits from an integrated European electricity market, we propose the following blueprint:

- First, we suggest adding a European system-management layer to complement national operation centres and help them to better exchange information about the status of the system, expected changes and planned modifications. The ultimate aim should be to transfer the day-to-day responsibility for the safe and economic operation of the system to the European control centre. To further increase efficiency, electricity prices should be allowed to differ between all network points between and within countries. This would enable throughput of electricity through national and international lines to be safely increased without any major investments in infrastructure.

- Second, to ensure the consistency of national network plans and to ensure that they contribute to providing the infrastructure for a functioning single market, the role of the European ten year network development plan (TYNDP) needs to be upgraded by obliging national regulators to only approve projects planned at European level unless they can prove that deviations are beneficial. This boosted role of the TYNDP would need to be underpinned by resolving the issues of conflicting interests and information asymmetry. Therefore, the network planning process should be opened to all affected stakeholders (generators, network owners and operators, consumers, residents and others) and enable the European Agency for the Cooperation of Energy Regulators (ACER) to act as a welfare-maximising referee. An ultimate political decision by the European Parliament on the entire plan will open a negotiation process around selecting alternatives and agreeing compensation. This ensures that all stakeholders have an interest in guaranteeing a certain degree of balance of interest in the earlier stages. In fact, transparent planning, early stakeholder involvement and democratic legitimisation are well suited for minimising as much as possible local opposition to new lines.

- Third, sharing the cost of network investments in Europe is a critical issue. One reason is that so far even the most sophisticated models have been unable to identify the individual long-term net benefit in an uncertain environment. A workable compromise to finance new network investments would consist of three components: (i) all easily attributable cost should be levied on the responsible party; (ii) all network users that sit at nodes that are expected to receive more imports through a line extension should be obliged to pay a share of the line extension cost through their network charges; (iii) the rest of the cost is socialised to all consumers. Such a cost-distribution scheme will involve some intra-European redistribution from the well-developed countries (infrastructure-wise) to those that are catching up. However, such a scheme would perform this redistribution in a much more efficient way than the Connecting Europe Facility’s ad-hoc disbursements to politically chosen projects, because it would provide the infrastructure that is really needed.

The Buzek Report acknowledges the need to move to joint network planning, better congestion management, converging incentives for the provision of capacity, ancillary services, and ‘greenness’, the need for a consistent market design and even proposes a cost socialisation scheme worth considering (point 27 refers to studying the possibility of a European levy for network investment). By the very nature of the report – it addresses a wider set of issues and is a compromise between many MEPs – it does, however, not provide a stringent vision itself.

Blueprint – ‚Borderless electricity: completing the internal energy market‚

[1] http://ec.europa.eu/energy/infrastructure/strategy/2020_en.htm